Follow Us

GK is a contributor to many traditional and non-traditional media outlets (CNBC, WSJ, Forbes, Bloomberg, Fox Business, etc.) and social media.

GK Original Shows

All Media

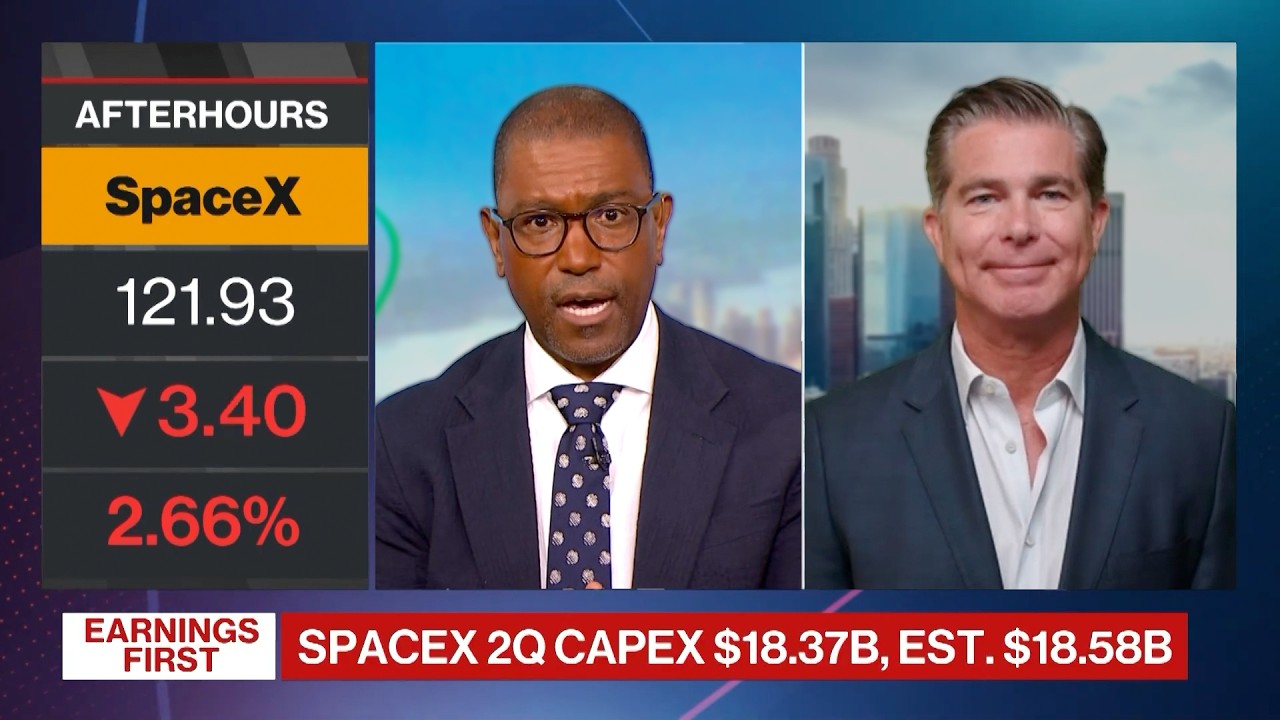

8/6/26

Ross Gerber - "There is no bubble" around A.I. | CNN

GK President and CEO Ross Gerber joins Jim Sciutto of CNN's The Brief to give his thoughts on the heavy CapEx spending at SpaceX, the growth opportunity for AI stocks, and why he's not concerned by Elon Musk splitting his leadership between three companies.

8/6/26

Ben Rosbach - SpaceX insiders get their first chance to cash out — but the stock’s slide will limit that opportunity | MarketWatch

SpaceX insiders are getting their first opportunity to cash out, but the biggest decision isn't whether you can sell, it's whether you should.

As the first lock-up period expires, MarketWatch turned to Gerber Kawasaki Wealth Advisor Ben Rosbach for insights on navigating volatility and the financial decisions employees may face as additional shares are unlocked.

Read the full article below!

8/5/26

Jimmy Bisharat - SpaceX Lock-Up: What Does Liquidity Mean for Me? | Gerber Kawasaki

What will you do when your SpaceX shares become liquid?

The answer isn't as simple as "sell" or "hold."

Gerber Kawasaki Wealth Advisor Jimmy Bisharat breaks down the key considerations every SpaceX employee should think through before making one of the biggest financial decisions of their career.

Read the full article below. 👇

8/5/26

Jimmy Bisharat - The First SpaceX Lockups are about to Expire. Now What? | Gerber Kawasaki

With the first in a series of SpaceX lockups is set to expire, insiders and employees are now faced with a difficult decision of what to do with their share of the hottest IPO of the decade. Wealth Advisor Jimmy Bisharat breaks down what to expect, and explains why the right move is often less obvious than simply holding or selling.

8/4/26

Zach Bainter - Did Your Health Plan Just Become HSA-Eligible? | Gerber Kawasaki

Did you know your Bronze or Catastrophic health plan might now qualify you for an HSA?

Thanks to a new provision in the One Big Beautiful Bill Act, more ACA marketplace plans are now HSA-eligible starting in 2026. This opens the door to a rare triple tax benefit: pre-tax contributions, tax-free growth, and tax-free withdrawals for medical expenses.

If you're on one of these plans, this could be a simple way to lower your taxable income while building long-term savings. Read more below👇

8/4/26

Ross Gerber - SpaceX is a Compelling Investment | Bloomberg

GK President and CEO Ross Gerber joins Bloomberg's Romaine Bostick to provide his instant reaction to the SpaceX Q2 earnings report, thoughts on the business relationship between SpaceX and Nvidia, and expectations for the future of the SpaceXAI datacenter buildout.

7/31/26

What is a Trump Account? 530A Explained | Gerber Kawasaki

This week, GK Managing Partner Ben Dunbar and Wealth Advisor Kaytlin Hall are teaming up to talk about the newest child savings plan on the block: the 530A Plan, or “Trump Account.” Together, they break down the benefits of saving early, explain who is eligible for the widely touted $1000 seed, and the downsides that parents should consider before opening an account.

7/30/26

Summer Reading Club: July Book - The Glass Castle by Jeannette Walls | Kaytlin Hall

Can a book about poverty teach us something about wealth?

This month's Summer Reading Club pick, The Glass Castle by Jeannette Walls, did exactly that.

In her latest review, Wealth Advisor Kaytlin Hall, MBA shares how this unforgettable memoir challenged her perspective as both a financial planner and a parent. While money can create opportunities, the story is a powerful reminder that resilience, stability, and the values we pass on can shape a family's future just as profoundly.

It's an emotional, thought-provoking read that sparked meaningful reflection, and we'd love to hear your thoughts.

7/29/26

Ayal Shmilovich - What the Dream Really Costs | Gerber Kawasaki

Travel ball isn't a season anymore, it's a budget line. In his latest article, Gerber Kawasaki Managing Partner Ayal Shmilovich, CPWA®, breaks down the real numbers behind youth travel baseball: from a single $10K Cooperstown week to the ten-year cost of the competitive path, and what that money could become if invested instead. It's not an argument against the sport, it's the honest math every sports parent deserves to see. Read more here.

7/29/26

Future Money Podcast: Prediction Market Mania

The dog days of summer are here, but that's no excuse to get caught sleeping on the market. Joined by special guest and GK Wealth Advisor Brett Sifling, Managing Partners Ayal Shmilovich and Hatem Dhiab are back in the studio to break down the wild conclusion to the World Cup, chart the next steps for SpaceX investors as the earliest lock-ups are set to expire, and question the integrity of the cryptocurrency and prediction market industries.

7/29/26

Chase McCormick - Your Budget Deserves A Vacation | Gerber Kawasaki

Saving and spending aren't enemies; they're partners. In his latest article, "Your Budget Deserves a Vacation," Wealth Planning Associate Chase McCormick shares a lesson he learned the hard way: discipline without purpose is just deprivation with extra steps. A refreshingly honest take on why your financial plan should leave room to actually enjoy your money, not just grow it.

7/28/26

Brett Sifling - Solana Prices Fall As Risk Aversion Pulls Crypto Markets Lower | Forbes

When crypto markets shake, people want answers, and Forbes came to Brett Sifling for them.

Brett, Wealth Manager at Gerber Kawasaki, was featured in Forbes breaking down Friday's Solana selloff. His take: stalled progress on the Clarity Act, bogged down by ethics disclosure fights, a stablecoin yield battle with banks, and DOJ concerns, is spooking crypto investors, compounded by rising oil prices, climbing treasury yields, and traders bracing for next week's Fed meeting.

This is the kind of clear, macro aware perspective Brett brings to every client relationship.